The soft cap iron condor:

My idea for this is basically a very skewed iron condor in certain conditions which aims to add a little premium or reduce max loss on a position at the chance of losing due to a huge vol collapse.Taking the existing portfolio risk of 10-20% max draw down with your short vol positions, we add verticals on the other side at about the 20% monthly decay mark which is about the max where VXX goes per month- the "soft cap". Those verticals aim to have a max loss equal to the max profit of the short vol verticals, meaning there is no risk of loss to the short vol side, but you theoretically could have a month ending up a scratch. In real trading conditions that much vol decay would have you rolling up/down the other side, but that complicates the simplified model.

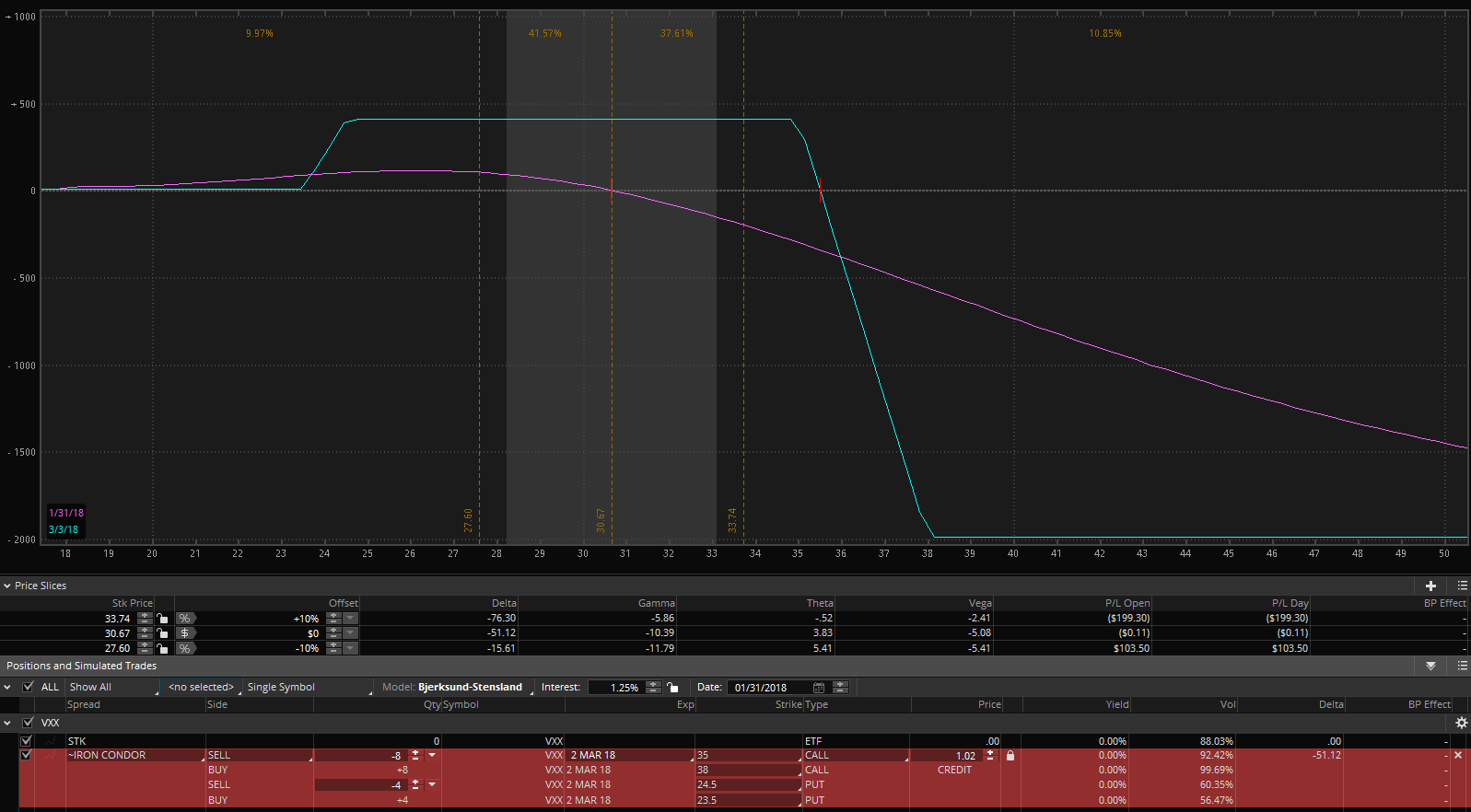

I was going to scribble this out in MSPaint but what is thinkorswim even for? Might as well make it look a little more accurate if we can. So here is the "soft cap iron condor" in VXX :

Assuming a sample 10k portfolio, targeting 20% max draw down from the short vol positions (verticals) we would have 2k max risk to play with-

Short side:

35/38 call spread (~15% out of the money) for .44 cr, $256 risk =~ 8 spreads

= $2048 risk, $352 credit

Normally this is where we would stop, but depending on spot VIX being super low, low spot with not much /VX premium over spot, or if your positions are at max loss and you want to take some max loss off, we add the skewed opposite side:

Long side:

$352 risk available, from the $352 credit from the short side

20% otm =~24.5 put

24.5/23.5= .13cr, 87 risk =~4 spreads

$348 risk, $52credit

Why is this different from $SPY iron condors?

Unlike straight stocks that have earnings, buyouts, crazy FOMO, short squeeze/melt ups, VIX products have some conceptual constraints which I was pointing to earlier such as the decay behavior in the 9 handle:

Conditions/issues:

-Obviously there is no free money anywhere so this is just a way to flatten risk and add more trade offs.

-I wouldn't do this right after a VIX spike because historically that is when you can hit those 20% monthly decay numbers (the quick VIX drop after a spike). I might add this on if after a VIX spike if all my other positions are max loss and you would be fine with a potential scratch for the month if it would take some max loss off.

-Obviously we won't be in the 9 handle forever so as spot VIX gets higher the 20% monthly breach risk goes up.

-It seems like the lower liquidity products (SVXY) almost factor this in and a lot of times the ~20% otm strike on the long vol credit side is the last one, meaning you can't make a vertical to reduce buying power reduction. For example even though most of my positions were SVXY short put spreads, a single 20% otm naked call was 20k BPR in Tastyworks.

-Due to the spread/liquidity issue, this type of trade might be confined to VXX. However, when dealing with such ~.12cr spread, depending on your broker the commissions really eat at those if you don't have some bulk pricing, so again this is really a marginal trade I wouldn't have always by default.

All of that being said, this might be a strategy to consider more as we go into a higher treasury yield/lower dollar environment where VIX might reach a new normal above the 10-11 handle that we saw for most of 2017. If we have more choppy market action then having a trade like this on might allow for single day VIX spike windows to take it off at a profit and look to re establish in a few days.